Case Study CPA

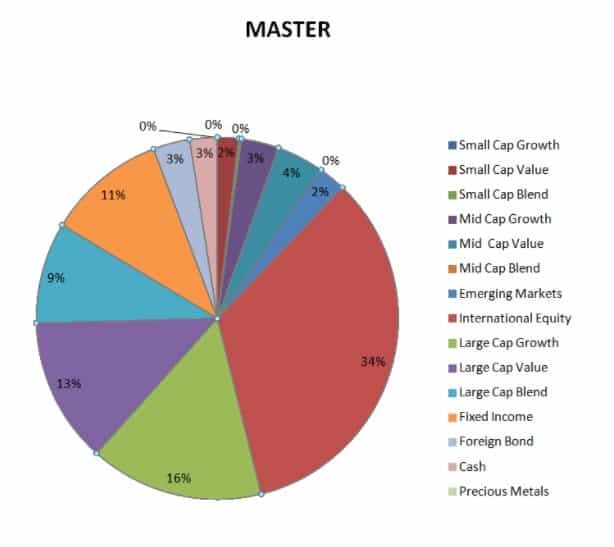

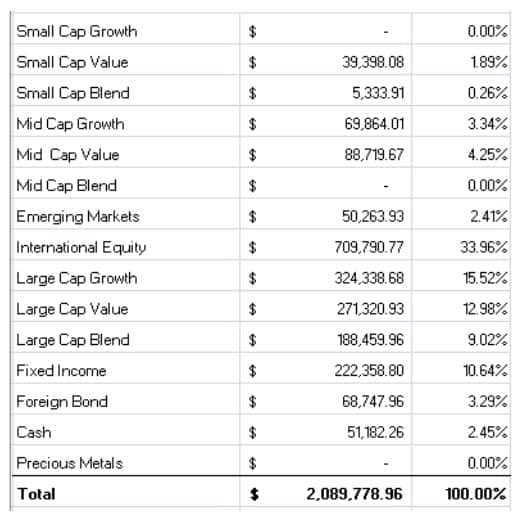

“James and Jane” are a fun couple. He is in his 70’s, and she is almost 60. They have six investment accounts, two IRA’s each, a joint account, and one account just in her name from an inheritance. Once of them is a CPA, and the accounts they held with their advisor seemed to be very well diversified. On detailed analysis – when we combined all positions in all accounts into one spreadsheet as part of our stress test, by researching each of the many, many positions and categorizing them into asset classes, then adding them up and graphing them as in in the spreadsheet and piechart below – a different picture emerged, as follows:

Almost 40% of the total allocation was in large cap US stocks, and 80% of the allocation to US stocks was in large caps. While the non-US allocation was reasonable, nearly none of it was in high potential growth areas like emerging markets, which include China (up about 40% so far this year as I write this), Korea, South America and other very promising areas. None of the non-US allocations were dollar-hedged, meaning that the strong dollar was eroding their potential profits significantly. Also, the fixed income allocation had a lot of junk bond funds when we dug deeper, which they said they did not know about.

It is important to note that the clients believed their advisor was working for only fees and putting them first, and they were quite surprised to learn that he was not in fact a fiduciary required to act in their best interests, and was taking commissions – some quite large but hard to spot – as well as fees. We find this situation to be quite common, and warn you that most “financial advisors” – including insurance agents, bank staff, and stockbrokers – are not fiduciaries, even though they appear to be – and you believe them to be – acting in your best interests. To be sure, insist that they tell you in writing that they are fiduciaries bound to put your interest first when managing investments.

There were other issues as well which we will discuss in the Case Study CPA sections to follow, and the cumulative effect was some pretty dramatic underperformance, which was so bad it will probably surprise you when we get to it. I stress that unless you are acutely tuned to it this can be very hard to spot – remember one of these clients was a CPA and used to financial analysis – but they still did not notice a very big difference from their growth and how well the market was doing overall.

They thought they were doing great, but sadly were doing quite poorly.

We should also note that while asset protection planning – techniques to outfox financial predators was very important to these folks, virtually none had been done by their advisor, with the result that a large portion of their wealth – well over a million in this case – was exposed to attack.

Case Study CPA

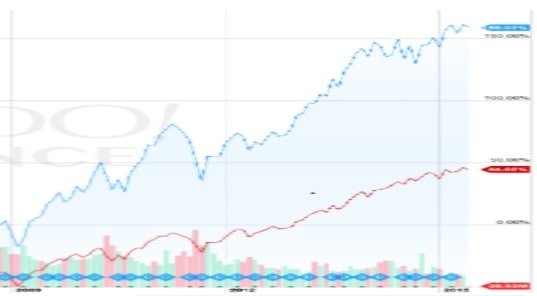

As we mentioned under Danger #2 when we reviewed the case study asset allocation, nearly 80% of the US stock allocation was in large caps; there was virtually none in US small caps. As can be seen in the graph below since the market bottom in March of 2009, this was an unfortunate oversight, with US small caps (represented by the blue line) handily outperforming the red-line S&P 500.

A more recent effect concerns the non-US allocation. There is nearly none in emerging markets, which we have mentioned we feel to be a big mistake. Also troubling was the fact that while there was a significant allocation to foreign stocks, the exposure was not currency-hedged during the recent period of US dollar strength; the short of it is that gains in non-US stocks were often canceled out by a rising dollar, with some periods actually showing net losses as the dollar went up more (making non-US stocks worth less in dollar terms) than the foreign markets. This could have easily been avoided with any number of dollar-hedged foreign stock mutual funds or ETF’s.

When we get to the performance discussion under Danger #6, you’ll see the devastating impact of these cumulative dangers on the couple in this case study.

Case Study CPA

Returning to the case study we looked at before the retiring doctor story, the total of portfolio construction miscues – selection, expenses, commissions, ongoing management (or lack thereof) and – resulted in some pretty disturbing underperformance. Before we did the Stress Test, these folks – again, one of whom is a CPA – thought they were doing pretty well, but the reality is actually somewhat heartbreaking.

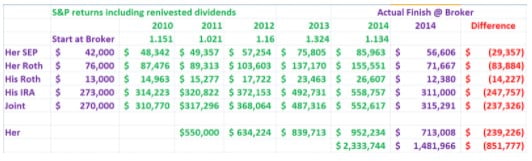

The spreadsheet below gives inferred performance for these client accounts based on the data they were able to provide. They told us there were no cash flows, so the beginning (Jan 1 2010 for all but one account) and the end values (Dec 31 2014) were clear. These are the purple numbers. In this case they asked us to compare performance to the S&P 500, so we took that annual return number (15.1% for 2010, for an appreciation factor of 1.151) to calculate “what if” values for each year in each account to emulate what the S&P 500 benchmark performance would have been. These are the green numbers. The bottom purple 2014 number ($1,481,966) was the total of their account values at the broker at the end of 2014, and the bottom green number ($2,333,744) would have been the total S&P 500 emulated value if that had been their performance. The bottom red number – $851,777 – is the difference between what they got and our hypothetical S&P 500 estimate. Nearly a million dollars difference in a five year span! Of course, this is not a rigorous academic analysis. For one thing, the data are too incomplete. For another, the investment asset allocation the broker had put them into did not match the S&P 500, but since this is such a popular benchmark, it gives some useful context.

Of course, this is not a rigorous academic analysis. For one thing, the data are too incomplete. For another, the investment asset allocation the broker had put them into did not match the S&P 500, but since this is such a popular benchmark, it gives some useful context.

These folks had thought they were doing far better than they did, and were pretty astonished to see the analysis above. They were also not too happy to learn about the commissions, mediocre rankings, and high expenses in many of their investments, and also to learn that there broker was not in fact a fiduciary who was acting in their best interests.

Your situation is probably somewhat different, and your available data may limit the observations we might make, but I can tell you the above situation is by no means unusual in our experience. If a CPA missed the big performance gap we noted above, is it possible you may have too in your portfolio planning?

Buying bonds is traditional considered a low risk investment activity, especially where highly-rated or US government bonds are concerned. The reason is simple: buy a bond from a solid source, and there is a very high probability that you will get what it promises – interest payments on time, and your money back when the bond matures. This “low risk” argument has always ignored two crucial factors, those being taxes, and inflation. When the toll that these two stealth risks take are tallied up, many bond investments produce net losses to their owners, in terms of purchasing power. There is a net decline in value in terms of real wealth. While this is not true for all investors in all markets, it is true often enough to be a cardinal rule to be remembered by all investors.

As we face the end of the near-zero interest rate era in the late twenty-teens, there is a very special case of this rule that looms as a disastrous risk for modern investors, driven by today’s low rates, and the current high risk of very high inflation. Both of these are a direct result of the “printing press” expansion of the US money supply, in the wake of the Great Recession. While these policies probably prevented a more severe contraction or even a Depression, these artificially low rates can’t hold forever without risking a very nasty surge of inflation, the likes of which has not been seen since the 1970’s in this country; even with rising rates, inflation is likely to be a much worse problem than it has for decades. Bear this in mind, as your mindset is probably not well prepared for this, having got used to low inflation for decades now.

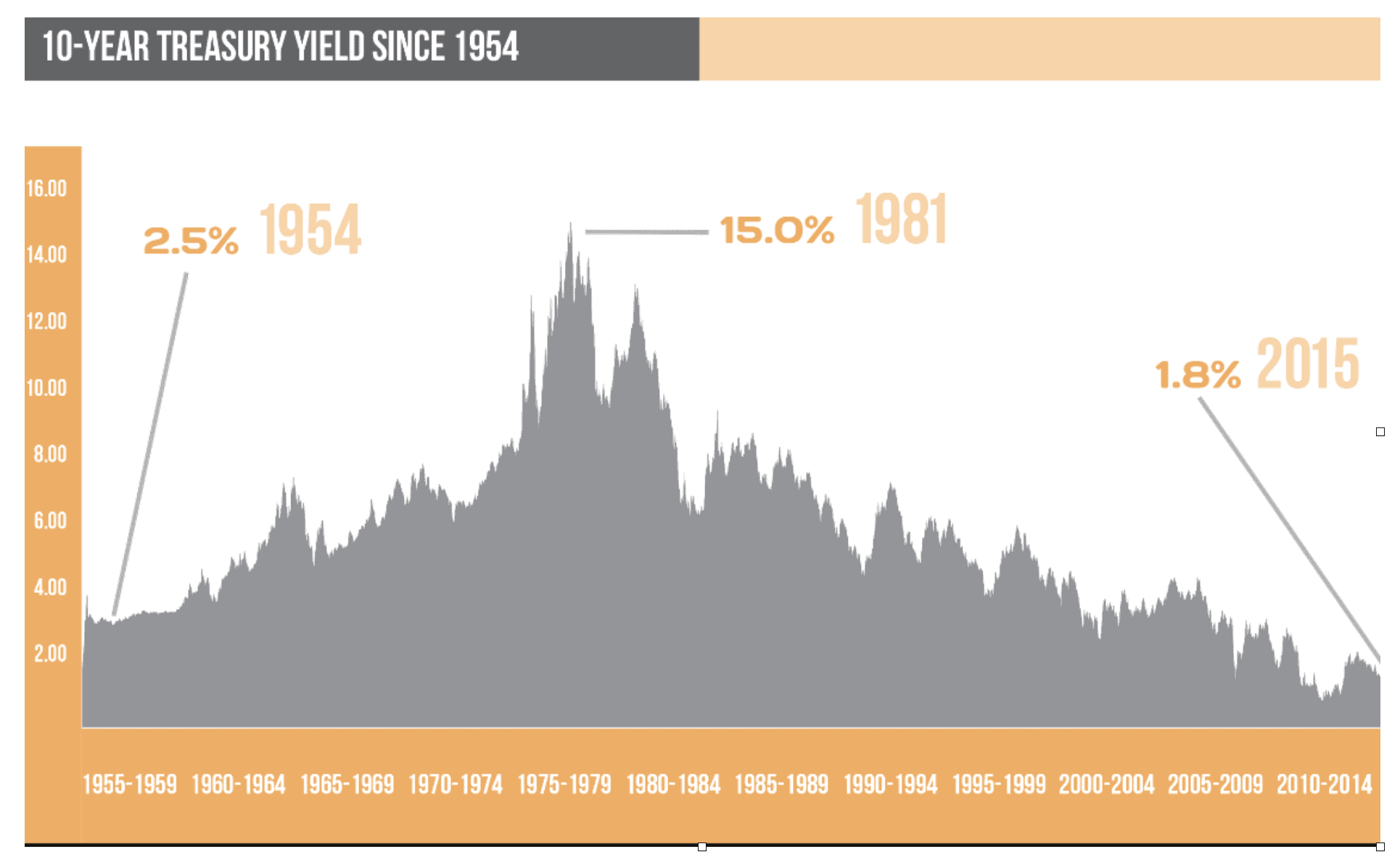

Worse yet, all of this sits on the powder keg of a likely bond-market bubble that has been building for thirty years. Have a look at the following graph, which charts interest rates on the US 10-year note. Bond prices move in the opposite direction of interest rates. Of course, most of us know intuitively that interest rates are very low now, and seem to have been falling, more or less, for a long time – since the high inflation days of the 1970’s. What is less obvious is that bond prices – which move in the opposite direction from interest rates – have been rocketing up for just as long, to levels that many fear have reached unsustainable “bubble” valuations. From the graph below, rates have been dropping since the late 1970’s, and bond prices have been rising since then, and now sit at near 40-years highs. When rates snap back – as they gradually did from the mid-50’s to the mid-70’s – bond losses, especially on longer term maturities, could be severe.

The short of it is that bond buyers/holders today face a huge problem beyond miniscule interest rates…the risk that values may tumble disastrously – in a macabre echo of the 2008 Stock Crash – if interest rates rise. For example, for a bond maturing in 10 years paying 2%, the value can drop by more than half if rates go to 12%…a million dollar investment could plunge to a market value of less than $450,000 in this simple example. There is more to it than that, of course, but this should make the big risks of buying bonds in a super-low interest rate environment quite clear. Note that this risk extends to market-adjusted (“MVA”) annuities and other “guaranteed” investments of the sort. The longer the term to maturity, the greater the risk of principal loss is. And while bond owners often take false comfort in their ability to hold until maturity and so get “all” their money back, the reality is that in doing so they miss the opportunity to invest at much higher interest rates along the way, and the loss – the true economic cost – turns out to be just about the same.

The other big risk to consider is default, the risk that the bond issuer will stiff you and not pay your money back. One must watch ratings carefully and regularly, and take them with a grain of salt. Remember that the “toxic waste” mortgage bonds that precipitated the Great Crash of 2008 came with investment-grade ratings, but turned out to be higher risk than junk bonds? Finally, note that bond funds are as exposed to these risks as individual bonds.

The short of it is that “conservative” bond investments may actually be quite risky in a risking interest rate environment, and that this risk is particularly acute in the mid-twenty-teens. It is difficult to overstate the potential magnitude of this risk in terms of purchasing power erosion, running out of money, or suffering big losses you may never be able to overcome. See the Case Study box for more detail. And, as an additional word of warning, many annuities have values tied to the bond market, and these risks affect them to varying degrees as well. If you have us do the below Stress Test, we can also help you assess any hidden risks in your annuities, if you have them.If you have (or are considering) bond positions, we will give you an objective evaluation as part of your free Portfolio Stress Test™, if you ask us to. If you are heavily into bonds, I cannot overemphasize how important I think assessing this risk is, and how dangerous to your financial security it could be.